Contract Analytics: Cordy Glenn | Terron Armstead | Josh Norman | Shawn Williams | Jordan Reed

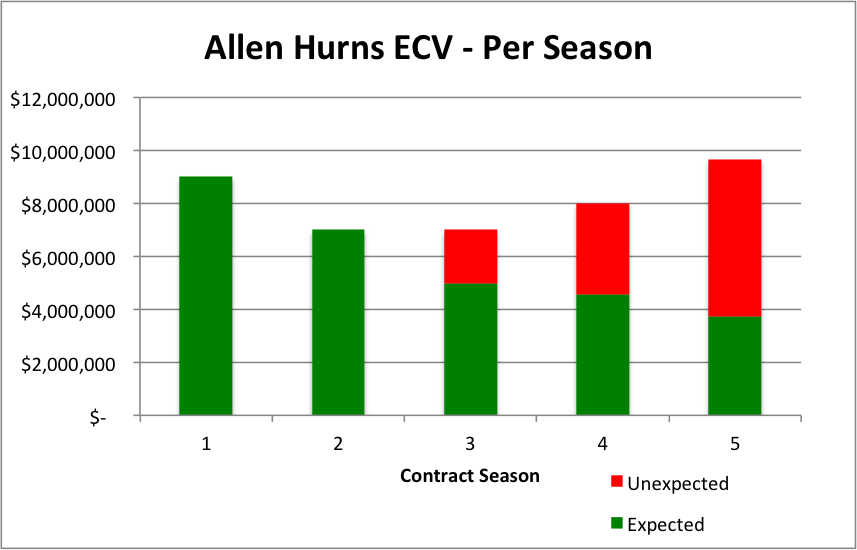

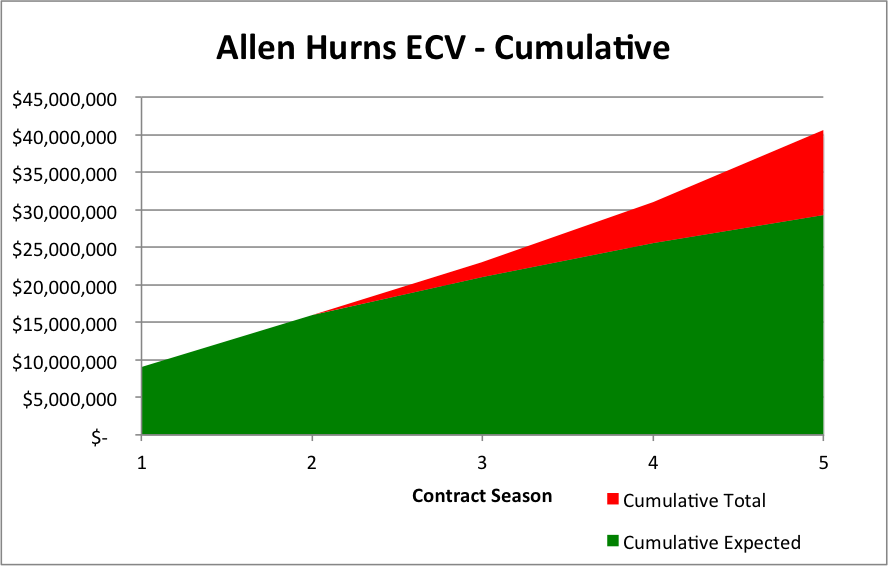

Allen Hurns signed a four-year extension with the Jaguars reportedly worth a face value of $40,650,000, of which $40.05 million is considered “new money” and $16 million is guaranteed at the time of signing. The Expected Contract Value of the deal is $29,261,110 (72% of face value):

| Allen Hurns |

| Face Value: $40,650,000 |

| Year | Salary | Expected Outcome | Expected Value | Guaranteed |

| 2016 | — | 99.0% | — | $9,000,000 |

| 2017 | — | 93.9% | — | $7,000,000 |

| 2018 | $7,000,000 | 71.2% | $4,984,649 | — |

| 2019 | $8,000,000 | 57.0% | $4,562,692 | — |

| 2020 | $9,650,000 | 38.5% | $3,713,770 | — |

| Subtotal | — | $13,261,110 | $16,000,000 |

| Expected Contract Value: | $29,261,110 (72%) |

Hurns has made a stronger tradeoff between securing guaranteed money in exchange for giving up free agency seasons than other players who have recently signed extensions, particularly due to the fact that he was subject to restricted free agency in 2017. Whereas other players (Jordan Reed, Terron Armstead, Harrison Smith) sacrificed 5 years of free agency despite being subject to only one season worth of team leverage, Hurns only sacrificed 3 years of free agency while being subject to two season’s worth of team leverage. In exchange, Hurns still secured more new guaranteed money than Reed or Smith and came relatively close to Armstead.

Because Hurns’ salary cap number increased by a significant amount in 2016, the contract remains largely flat on the back end, which helps to prop up the Expected Outcomes in 2019 and 2020 despite the lack of dead money protection. An Expected Contract Value of 72% of face value is slightly above average, although it is worth noting that Randall Cobb’s Expected Contract Value is $31.58 million (79% of face value). This further goes to show that slightly surpassing the APY of another contract is meaningless if the structure is not as strong.

In order to analyze the advantages and disadvantages of the contract from the team’s perspective, one must first identify the amount of money that Hurns’ production would be worth in 2016 on a one-year, fully guaranteed contract. I will refer to this amount as the player’s “Intrinsic Value.” Intrinsic Value may differ from market value for a variety of reasons, most notably the leverage of the respective parties. It is unclear at this point in time how an NFL player’s Intrinsic Value would be precisely calculated, as no WAR-like metric currently exists, but it should be theoretically possible to assign an Intrinsic Value to each player’s production. Once the determination of Intrinsic Value has been made, then the anticipated surplus value (or lack thereof) relative to Intrinsic Value can be compared to the risk incurred and optionality secured by the team.

Although I make no assertions as to Hurns’ Intrinsic Value, for the purposes of this analysis let’s assume the number to be $10 million, for no other reason that this is the number that has been heavily advertised as the “new money APY.” If we assume modest increases in the salary cap of 5% per year, then Hurns’ Intrinsic Value throughout the contract would be approximately $10M (2016), $10.5M (2017), $11.025M (2018), $11.57M (2019) and $12.155M (2020). Compared to his cap numbers, the team would potentially realize surplus value in the amounts of $1M (2016), $3.5M (2017), $4.025M (2018), $3.57M (2019) and $2.505M (2020).

However, the probability of the team realizing the surplus value is not the same in each season of the contract. Hurns may suffer injuries or performance decline throughout the contract that may cause the team to determine that releasing him and preserving the associated salary cap space would be the more efficient allocation of that salary cap space. In order to capture these considerations, we must now apply the Expected Contract Value probabilities to the potential surplus value of each contract season.

| Season | Estimated Intrinsic Value | Salary Cap Number | Potential Surplus | Contract Expectation | Expected Surplus |

| 2016 | $10,000,000 | $9,000,000 | $1,000,000 | 99.0% | $990,000 |

| 2017 | $10,500,000 | $7,000,000 | $3,500,000 | 93.9% | $3,286,500 |

| 2018 | $11,025,000 | $7,000,000 | $4,025,000 | 71.2% | $2,865,800 |

| 2019 | $11,570,000 | $8,000,000 | $3,570,000 | 57.0% | $2,034,900 |

| 2020 | $12,155,000 | $9,650,000 | $2,505,000 | 38.5% | $964,425 |

| Total | | | | $10,141,625 |

So if we assume that Hurns’ Intrinsic Value for 2016 is $10 million, then the team would expect to capture roughly $10.14 million worth of surplus value over the life of the contract. If we assume that the Intrinsic Value is $8 million, then the expected surplus value would be less. If we assume the Intrinsic Value is $12 million, then the expected surplus value would be greater.

In order to manufacture this expected surplus value, the team incurred $15.4 million worth of risk, which amounts to the $16 million worth of fully guaranteed money less the $600K base salary scheduled for 2016. While it is highly likely that Hurns would have received one of the larger RFA tenders in 2017, the fact is that no 2017 tender was guaranteed as of the time of signing this extension.

In addition to manufacturing $10.14 million worth of expected surplus value and incurring $15.14 million worth of risk, the team also secured some amount of optionality. To illustrate, as of February 2018, the team will be able to choose whether to retain Hurns for the 2018 season with no ongoing risk and without paying market value (which may exceed the Intrinsic Value). While there may be surplus value associated with the $7 million 2018 salary cap number, this team option in 2018 carries value even if Hurns’ Intrinsic Value in 2018 is precisely $7 million. This is because if the team was forced to sign Hurns to a new contract as a free agent in 2018, it would almost certainly have to incur new risk (likely spread over multiple years) and it would likely pay a market value greater than $7 million.

As a result, in each of 2018, 2019 and 2020, the team derives value from the fact that it can pick up the team option without incurring any additional risk and without paying market value. The potential to derive this type of value in a future year is incorporated into Expected Contract Value calculations in any given year. As a result, this optionality value is smaller with respect to the 2019 contract season than the 2018 contract season, and even smaller for the 2020 contract season.

Whether manufacturing $10.14 million worth of expected surplus value and securing some undetermined quantity of optionality value was worth incurring $15.4 million worth of risk is difficult to say at this point in time, as I have not yet applied this analysis to enough deals to get a sense as to where this fits within the entire universe of contracts. However, I think that this type of analysis is the most objective method to analyze contract from the team perspective.

From a team-wide perspective, this contract contributes to Jacksonville’s climb up the Commitment Index rankings this offseason, as it moves the team from 22nd to 13th. The team’s Commitment Index score is now 95, which means that it is 95% as committed to its current roster as a theoretical average team possessing the same degree of net true commitment as the mean of all 32 teams.

However, most of this commitment is attributable specifically to 2017, as the team now possesses the 7th least amount of True Cap Space in 2017. It is worth noting, though, that a large majority of Jacksonville’s 2017 true commitments come in the form of fully guaranteed base salary, rather than prorated signing bonus amounts. This means that the commitment is tradable to the extent that other teams are willing to accept players at least for free (as opposed to demanding that the Jaguars provide compensation). Given the trades that Philadelphia executed this offseason, the market for offloading unwanted guaranteed base salaries seems robust.

As a result, the Jaguars are in a position to continue extending other prominent young players over the next year or so, as the true commitments for such extensions will overlap with the true commitments of existing contracts to only a small degree, and the team is therefore far from being in a position of compromised flexibility.

| Allen Hurns |

| Year | Cap Number | Probability | Dead Money | Probability | Expected Cap Number |

| 2016 | $9,000,000 | 99.0% | $16,000,000 | 1.0% | $9,070,000 |

| 2017 | $7,000,000 | 93.9% | $7,000,000 | 6.1% | $7,000,000 |

| 2018 | $7,000,000 | 71.2% | $0 | 28.8% | $4,984,649 |

| 2019 | $8,000,000 | 57.0% | $0 | 43.0% | $4,562,692 |

| 2020 | $9,650,000 | 38.5% | $0 | 61.5% | $3,713,770 |

| Total: | | | | $29,331,110 |

Expected Contract Value was created by Bryce Johnston and Nick Barton.

Bryce Johnston earned his Juris Doctor from Georgetown University Law Center in May 2014, and currently works as a corporate M&A associate in the New York City office of an AmLaw 50 law firm. Before becoming a contributor to overthecap.com, Bryce operated eaglescap.com for 10 NFL offseasons, appearing multiple times on 610 WIP Sports Radio in Philadelphia as an NFL salary cap expert. Bryce can be contacted via e-mail at bryce.l.johnston@gmail.com or via Twitter @NFLCapAnalytics.

Nick Barton is a junior at the McDonough School Business at Georgetown University. He is majoring in Finance and Operations and Information Management. Nick currently interns with an NFL team . His prior work experience includes interning with CollegeSplits and Dynamic Sports Solutions, and working as a research assistant for the Center of Applied Research of the Apostolate.