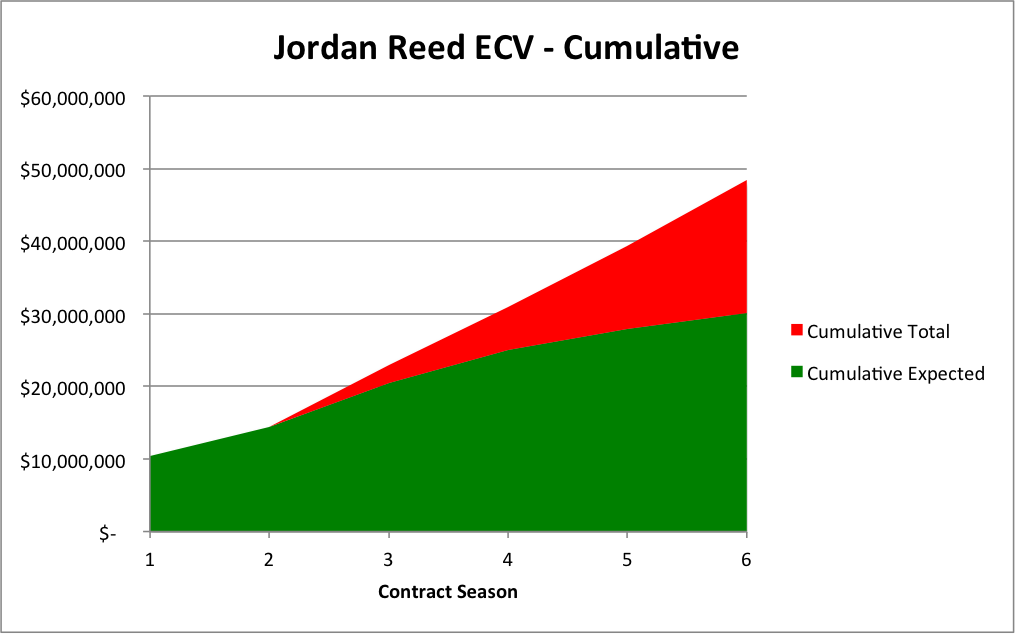

Jordan Reed signed a five-year extension with Washington reportedly worth a stated value of $48,389,750, of which $46.75 million is considered “new money” and $14 million is guaranteed at the time of signing. The Expected Contract Value of the deal is $30,118,560 (62% of the stated value):

| Jordan Reed |

| Stated Value: $48,389,750 |

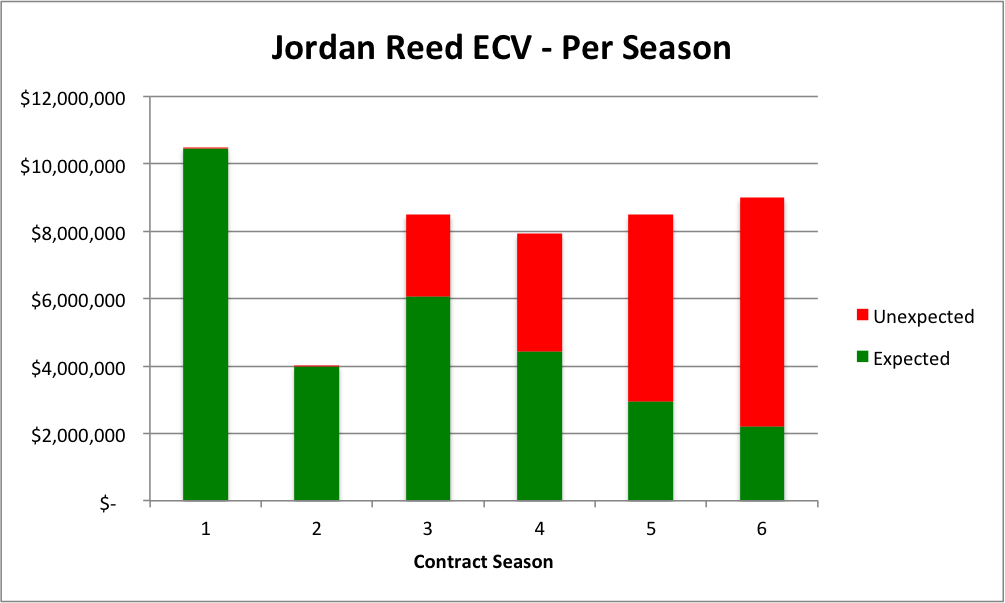

| Year | Salary | Expected Outcome | Expected Value | Guaranteed |

| 2016 | $218,750 | 99.4% | $217,336 | $10,250,000 |

| 2017 | $250,000 | 96.9% | $242,331 | $3,750,000 |

| 2018 | $8,500,000 | 71.4% | $6,069,615 | — |

| 2019 | $7,921,000 | 56.1% | $4,440,600 | — |

| 2020 | $8,500,000 | 34.7% | $2,948,937 | — |

| 2021 | $9,000,000 | 24.4% | $2,199,741 | — |

| Subtotal | — | $16,118,560 | $14,000,000 |

| Expected Contract Value: | $30,118,560 (62%) |

Every NFL contract consists of three fundamentals that are influenced by the specific structure of the contract: risk, upside, and optionality. Risk is largely a function of fully guaranteed money. As more fully guaranteed money is included in a contract, the team assumes more risk and the player assumes less risk. Upside is largely a function of the total amount of money. As more total money is included in the contract, the team obtains less upside and the player obtains more upside. Optionality is largely a function of the number of non-guaranteed contract seasons. As more non-guaranteed contract seasons are included in a contract, the team secures more optionality and the player forfeits optionality. In each case, the inverse is true as the contract structure moves in the opposite direction.

Each contract must be analyzed within the context of these fundamentals, and it is reasonable to expect that in any given contract negotiation one party may focus on designing a contract structure that strengthens one fundamental from that party’s perspective in exchange for weakening one or both of the other fundamentals. It is important to keep this in mind in order to avoid over-focusing the analysis on just one of the fundamentals.

This particular contract appears to favor Reed in terms of upside, while favoring Washington in terms of risk and optionality. I do not purport to possess any expertise or insight that would allow me to rank the positioning of a given player within the hierarchy of players at his position, so I cannot speak to whether Reed “deserves” a larger contract than Zach Ertz or Travis Kelce or Jimmy Graham or any other tight end. However, the fact that Reed’s contract ranks 3rd among all tight end contracts in both total new money and total APY despite it not being obvious whether Reed is among the three best tight ends in the league suggests that the upside of this contract is favorable for him. The flip side is that this contract does not present Washington with a lot of upside in terms of potential for surplus value.

However, the team appears to have done well for itself in terms of both minimizing risk and maximizing optionality. For a contract of this size, $14 million worth of fully guaranteed money is not a large number. Washington did not surrender a guaranteed third contract season or an Accelerated Future Team Option Deadline for the third contract season. Reed’s $9 million signing bonus is a manageable number that does not present a large amount of potential dead money in the third contract season and beyond, and Reed’s small cap numbers in the first two contract seasons minimize the likelihood that the team will want to execute cap-driven restructures that would push more dead money protection into the later year’s of the contract. All of these factors are baked into the application of the Expected Contract Value model to this contract, the result of which is that Reed can only expect to earn roughly 62% of the total value of the contract. This expectation is comfortably below the average of all contracts for which I have calculated ECV.

Washington maximizes optionality in two ways. First, Reed’s cap numbers for 2016 and 2017 are well below the APY of the deal, which means that the team preserves the ability to allocate the difference elsewhere. Second, the team possesses options on four seasons (2018-2021) worth of nonguaranteed contract seasons. The “buyout” associated with not exercising these options – the dead money resulting from prorated signing bonus amounts – begins at $5.4 million in 2018 and drops to $3.6 million in 2019 and $1.8 million in 2020 before exhausting in advance of the 2021 team option. So while the lack of upside associated with any of these team options may be minimal, the team will at least have the flexibility to reevaluate each year based on Reed’s performance and health during the preceding season.

One must wonder if Reed would have been better off going in the opposite direction with the contract by sacrificing upside to maximize optionality. For example, perhaps the team would have agreed to an extension of only two seasons (through 2018) at an APY of $6 million or $7 million per season. In this example Reed would have received less money during 2016-2018 than in the deal he actually signed, but he would have had the opportunity to return to free agency in 2019 prior to his age-29 season with the opportunity to far exceed the contract amounts now scheduled for 2019-2021. Perhaps Reed and his agent proposed such an alternative structure to Washington and were met with significant resistance. Either way, these are the types of considerations that both parties should consider during negotiation.

This contract moves Washington into 4th place in Commitment Index with a score of 187, which means the team is responsible for 87% more future salary cap commitments net of current salary cap space than the average team. This metric only takes into account true commitments (prorated signing bonus amounts and fully guaranteed salary), as opposed to scheduled salary cap numbers of players under contract. If Washington signs Kirk Cousins to an extension, the team will most likely end up with the highest Commitment Index score in the league, which means the team will have less flexibility than every other team. A lack of flexibility does not necessarily lead to a lack of success, as commitment to a successful roster should be seen as a good situation. However, given that in the NFL performance is difficult to measure and predict, significant injuries occur with regularity, and team performance ebbs and flows on the basis of both controllable and uncontrollable factors, maintaining the salary cap flexibility necessary to make roster changes without incurring a net loss of talent remains desirable.

| Jordan Reed |

| Year | Cap Number | Probability | Dead Money | Probability | Expected Cap Number |

| 2016 | $3,406,028 | 99.4% | $14,137,278 | 0.6% | $3,470,416 |

| 2017 | $5,800,000 | 96.9% | $10,950,000 | 3.1% | $5,959,650 |

| 2018 | $10,300,000 | 71.4% | $5,400,000 | 28.6% | $8,898,600 |

| 2019 | $9,721,000 | 56.1% | $3,600,000 | 43.9% | $7,033,881 |

| 2020 | $10,300,000 | 34.7% | $1,800,000 | 65.3% | $4,749,500 |

| 2021 | $9,000,000 | 24.4% | $0 | 75.6% | $2,196,000 |

| Total: | | | | $32,308,047 |

Expected Contract Value was created by Bryce Johnston and Nick Barton.

Bryce Johnston earned his Juris Doctor from Georgetown University Law Center in May 2014, and currently works as a corporate M&A associate in the New York City office of an AmLaw 50 law firm. Before becoming a contributor to overthecap.com, Bryce operated eaglescap.com for 10 NFL offseasons, appearing multiple times on 610 WIP Sports Radio in Philadelphia as an NFL salary cap expert. Bryce can be contacted via e-mail at bryce.l.johnston@gmail.com or via Twitter @NFLCapAnalytics.

Nick Barton is a junior at the McDonough School Business at Georgetown University. He is majoring in Finance and Operations and Information Management. Nick currently interns with an NFL team . His prior work experience includes interning with CollegeSplits and Dynamic Sports Solutions, and working as a research assistant for the Center of Applied Research of the Apostolate.