Today I would like to explore the impact different state and city tax rates have on teams and players across the league. I have seen articles that broached this topic but usually limited it to “California has a 13.3% income tax and Florida has no income tax, so California teams have 13.3% less to work with than Florida teams”. While this is directionally accurate, it is a vast oversimplification. Below I’m going to go into more detail on two tax-related issues: the differing purchasing powers of each NFL team, and analyzing a few free agency moves from earlier this year to show how state taxes may impact a player’s decision.

General Rules & Assumptions

Before I get into the details, I would like to clarify a few assumptions I have made as well as some general tax facts.

- All earnings are taxed based on the location where the earnings are realized. Colorado’s income tax rate is 4.63%. This does not mean that all of Denver’s players are taxes at 4.63% year-round. When the Broncos play the Raiders in Oakland, all of Denver’s players are taxed at the California rate of 13.3% for that week’s game check.

- All earnings are taxed at the highest tax bracket. The IRS and each state designs their tax rates to gradually rise as an individual’s income rises. As the IRS’s top bracket is income over $466,950 – lower than the NFL minimum, for the purposes of easier calculations, I’m going to assume all earnings are at the highest rate in each state.

- Some cities, counties, and townships have taxes on top of state and federal taxes. I have included the local jurisdiction taxes where available. Where two rates were present (usually resident vs non-resident), I used the higher rate.

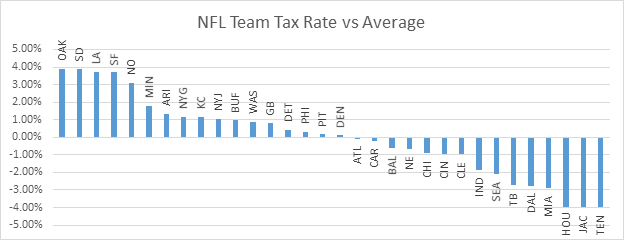

NFL Team Purchasing Power

Purchasing power is usually a term used to compare the purchasing ability of single persons in two different countries or two different markets within a single country – consider the difference in the cost of living between New York and Green Bay. To determine each NFL team’s total purchasing power, I’m going to look at how much each team’s roster’s total after-tax cash is impacted by the tax rates in the cities it plays in year after year. For this exercise, I assumed that each NFL team plays 8 games in its own stadium, 1 in each of its division opponent’s stadium, 2 away games in the NFC, 2 away games in the AFC, and one of its two conference strength of schedule games in an away city. Each team’s average tax rate was then compared to the league average tax rate to determine an approximation of how much of an advantage or disadvantage each team has.

Miami’s detailed calculation is shown below. Even though Florida doesn’t have an income tax, the Dolphins travel out of state for up to 8 games a year, bringing each Dolphins player’s estimated state tax rate up to approximately 3.36%. While this is higher than if all games were played in Miami, each Dolphins player is still taxed at around 2.87% less than the league average.

| MIA | |

| Game Site | Tax Rate |

| MIA | 0.00% |

| MIA | 0.00% |

| MIA | 0.00% |

| MIA | 0.00% |

| MIA | 0.00% |

| MIA | 0.00% |

| MIA | 0.00% |

| MIA | 0.00% |

| NYJ | 8.97% |

| NE | 5.10% |

| BUF | 8.82% |

| NFC Away | 6.53% |

| NFC Away | 6.53% |

| AFC Away | 5.94% |

| AFC Away | 5.94% |

| Conf Away | 5.94% |

| Blended Rate | 3.36% |

| Vs Avg | -2.87% |

**Update 10/5/16: The above example for Miami as well as the below chart showing all teams depict a team’s average state tax rate across several years, not specifically 2016. Miami players may not incur exactly 3.36% in state taxes in every year, but when several years are considered together, they should average out to around 3.36%. The below chart does not show the state tax rate for each team’s home stadium. Instead, it shows how each team’s blended state tax rate compares to the league average. The blended state tax rate is the rate players will incur as they play 8 home game and 8 away games each season.**

While the tax rates by team vary from 0% to 13.3%, the blended rate when considering game sites reduces the impact to +/- 4% different than the league average. Teams on the lower (negative) end of the spectrum have more purchasing power. Their players incur less tax expense, which means that $1 paid to them from their existing team is worth more than $1 paid to them by another team.

Teams can further manipulate tax discrepancies by assigning larger or smaller portions of payments into signing bonuses or salaries. Consider Ndamukong Suh’s recent contract with the Miami Dolphins which included a $25.5M signing bonus. Let’s assume that Detroit was offering an identical offer to Miami’s. In Detroit, the signing bonus would have been taxed at 6.75%, which means Suh would have incurred $1.72M in state taxes. From an after-tax point of view, the seemingly identical offers wouldn’t have been equal because Detroit’s offer was the same pre-tax, but $1.72M less after taxes.

2016 Free Agency

Each time a free agent signs with a different team, we don’t know if taxes were a consideration. We also don’t know what the competing offers were that were eventually turned down. However, that doesn’t need to stand in the way of comparing free agent contracts against hypothetical identical offers from the player’s original team. Below, I’m going to consider the difference in three year cash flows in two scenarios where the new team’s rate is higher than the original team and in two scenarios where it is lower. Keep in mind that the only taxes shown are state and local taxes as the remainder of taxes are identical across the country.

First up: Malik Jackson. Jackson signed a 6 year, $85.5 million contract with $31.5 million fully guaranteed and a $10 million signing bonus. Assuming the Broncos were offering an identical contract, Jackson saved $1.7 million by signing with Jacksonville.

| Malik Jackson (JAC) | |||||

| Year 1 | Year 2 | Year 3 | |||

| Yr 1 Avg Tax % | 2.46% | Yr 2 Avg Tax % | 2.18% | Yr 3 Avg Tax % | 1.92% |

| Yr 1 Salary | $8,000,000 | Yr 2 Salary | $13,500,000 | Yr 3 Salary | $13,500,000 |

| Yr 0/1 Bonus | $10,000,000 | Yr 2 Bonus | Yr 3 Bonus | ||

| Bonus Tax % | 0.00% | Bonus Tax % | Bonus Tax % | ||

| Yr 1 Total Tax | $197,100 | Yr 2 Total Tax | $294,718 | Yr 3 Total Tax | $258,588 |

| 3 Year Tax Total | $750,406 | ||||

| Malik Jackson (DEN) | |||||

| Year 1 | Year 2 | Year 3 | |||

| Yr 1 Avg Tax % | 5.04% | Yr 2 Avg Tax % | 5.53% | Yr 3 Avg Tax % | 6.22% |

| Yr 1 Salary | $8,000,000 | Yr 2 Salary | $13,500,000 | Yr 3 Salary | $13,500,000 |

| Yr 0/1 Bonus | $10,000,000 | Yr 2 Bonus | Yr 3 Bonus | ||

| Bonus Tax % | 4.63% | Bonus Tax % | Bonus Tax % | ||

| Yr 1 Total Tax | $866,185 | Yr 2 Total Tax | $746,803 | Yr 3 Total Tax | $839,168 |

| 3 Year Tax Total | $2,452,157 | ||||

In order for Denver to offer an equal after-tax contract, they would need to increase their three year cash by slightly over the same $1.7 million. Assuming that additional amount was entirely in the signing bonus, it would have increased the APY by $283 thousand and the cap hit by $340 thousand over the first five years of the contract.

A second high profile Denver exit was Brock Osweiler. Osweiler signed a 4 year, $72 million contract with $37 million fully guaranteed and a $12 million signing bonus. Osweiler also has a $5 million roster bonus in the first year. Again assuming an identical offer by the Broncos, Osweiler saves $2.15 million by signing with Houston.

| Brock Osweiler (HOU) | |||||

| Year 1 | Year 2 | Year 3 | |||

| Yr 1 Avg Tax % | 2.74% | Yr 2 Avg Tax % | 2.07% | Yr 3 Avg Tax % | 2.23% |

| Yr 1 Salary | $4,000,000 | Yr 2 Salary | $16,000,000 | Yr 3 Salary | $18,000,000 |

| Yr 0/1 Bonus | $17,000,000 | Yr 2 Bonus | Yr 3 Bonus | ||

| Bonus Tax % | 0.00% | Bonus Tax % | Bonus Tax % | ||

| Yr 1 Total Tax | $109,575 | Yr 2 Total Tax | $330,695 | Yr 3 Total Tax | $402,159 |

| 3 Year Tax Total | $842,429 | ||||

| Brock Osweiler (DEN) | |||||

| Year 1 | Year 2 | Year 3 | |||

| Yr 1 Avg Tax % | 5.04% | Yr 2 Avg Tax % | 5.53% | Yr 3 Avg Tax % | 6.22% |

| Yr 1 Salary | $4,000,000 | Yr 2 Salary | $16,000,000 | Yr 3 Salary | $18,000,000 |

| Yr 0/1 Bonus | $17,000,000 | Yr 2 Bonus | Yr 3 Bonus | ||

| Bonus Tax % | 4.63% | Bonus Tax % | Bonus Tax % | ||

| Yr 1 Total Tax | $988,693 | Yr 2 Total Tax | $885,100 | Yr 3 Total Tax | $1,118,891 |

| 3 Year Tax Total | $2,992,684 | ||||

Denver wasn’t the only team losing free agents and not all free agents signed with teams in 0% tax states. Olivier Vernon and Kelechi Osemele signed massive free agent deals with teams in higher than average tax states.

OIivier Vernon signed a 5 year, $85 million contract with $40 million fully guaranteed and a $20 million signing bonus. Vernon also has a $7 million roster bonus in the first year. An identical contract with Miami would have netted Vernon $3.33 million more after taxes.

| Olivier Vernon (NYG) | |||||

| Year 1 | Year 2 | Year 3 | |||

| Yr 1 Avg Tax % | 7.47% | Yr 2 Avg Tax % | 7.55% | Yr 3 Avg Tax % | 6.52% |

| Yr 1 Salary | $1,750,000 | Yr 2 Salary | $11,250,000 | Yr 3 Salary | $12,750,000 |

| Yr 0/1 Bonus | $27,000,000 | Yr 2 Bonus | Yr 3 Bonus | ||

| Bonus Tax % | 8.97% | Bonus Tax % | Bonus Tax % | ||

| Yr 1 Total Tax | $2,552,545 | Yr 2 Total Tax | $849,287 | Yr 3 Total Tax | $830,782 |

| 3 Year Tax Total | $4,232,614 | ||||

| Olivier Vernon (MIA) | |||||

| Year 1 | Year 2 | Year 3 | |||

| Yr 1 Avg Tax % | 3.76% | Yr 2 Avg Tax % | 3.82% | Yr 3 Avg Tax % | 3.18% |

| Yr 1 Salary | $1,750,000 | Yr 2 Salary | $11,250,000 | Yr 3 Salary | $12,750,000 |

| Yr 0/1 Bonus | $27,000,000 | Yr 2 Bonus | Yr 3 Bonus | ||

| Bonus Tax % | 0.00% | Bonus Tax % | Bonus Tax % | ||

| Yr 1 Total Tax | $65,884 | Yr 2 Total Tax | $430,179 | Yr 3 Total Tax | $405,856 |

| 3 Year Tax Total | $901,920 | ||||

Kelechi Osemele signed a 5 year, $58.5 million contract with $25.4 million fully guaranteed. $12 million of the full guaranty is spread between $6 million roster bonuses in each of the first two years of the contract. An identical contract with Baltimore would have netter Osemele $1.87 million more after taxes.

| Kelechi Osemele (OAK) | |||||

| Year 1 | Year 2 | Year 3 | |||

| Yr 1 Avg Tax % | 8.88% | Yr 2 Avg Tax % | 9.33% | Yr 3 Avg Tax % | 10.29% |

| Yr 1 Salary | $6,700,000 | Yr 2 Salary | $6,700,000 | Yr 3 Salary | $9,700,000 |

| Yr 0/1 Bonus | $6,000,000 | Yr 2 Bonus | $6,000,000 | Yr 3 Bonus | |

| Bonus Tax % | 13.30% | Bonus Tax % | 13.30% | Bonus Tax % | |

| Yr 1 Total Tax | $1,392,960 | Yr 2 Total Tax | $1,422,775 | Yr 3 Total Tax | $998,127 |

| 3 Year Tax Total | $3,813,862 | ||||

| Kelechi Osemele (BAL) | |||||

| Year 1 | Year 2 | Year 3 | |||

| Yr 1 Avg Tax % | 5.13% | Yr 2 Avg Tax % | 5.38% | Yr 3 Avg Tax % | 5.71% |

| Yr 1 Salary | $6,700,000 | Yr 2 Salary | $6,700,000 | Yr 3 Salary | $9,700,000 |

| Yr 0/1 Bonus | $6,000,000 | Yr 2 Bonus | $6,000,000 | Yr 3 Bonus | |

| Bonus Tax % | 5.75% | Bonus Tax % | 5.75% | Bonus Tax % | |

| Yr 1 Total Tax | $688,811 | Yr 2 Total Tax | $705,634 | Yr 3 Total Tax | $553,773 |

| 3 Year Tax Total | $1,948,217 | ||||

Other Considerations

This exercise is not meant to conclude that players are selecting free agent destinations based on tax rates alone. I don’t believe Osweiler chose Houston over Denver solely because he saved over $2 million in taxes. There are many other considerations in free agency – scheme fit, starting role, coaching staff, and the team’s playoff changes are some on the player side. The team has additional considerations such as cap space. However, in light of recent free agents admitting that their move to a new team was primarily motivated by money – Byron Maxwell is one example – a team can have an edge over its competitors if its state and city tax rates are significantly lower.