My recent article on state tax rates created enough follow-up questions that I would like to clarify in more space than is feasible for the comments section. I am not an expert in any of these areas, so please note in the comments section if my research has missed something.

In no particular order:

What are the tax (or other) implications for a team that moves to London?

Let’s assume that the Jaguars relocate to London. The team would maintain its existing incorporation in Florida (where I assume they are currently registered) and would create a wholly owned subsidiary in the UK. All players would be signed by the Florida-based employer. The team would have UK employees (marketing/sales, game day staff, etc), but all players would be employed out of the US. The UK allows for foreign citizens to come to the UK for business meetings and conferences without paying UK taxes. I haven’t been able to find definitive evidence to conclude that NFL players would also fall into this category.

Continuing with the Jaguars example, let’s assume that the team would hold all possible team functions in the US: training camp, mini camps, rookie camp, practices before US-based away games. If the team stays in the UK from Monday through Sunday for games in London, the players would spend a minimum of 8 weeks in London. To increase the local fan base, the team would most likely hold part or all of training camp in the UK, so I’m going to assume that players would spend up to 12 weeks in London. The remaining time on the NFL calendar would be taxes somewhere in the US (either in Florida at the Jaguar’s facility or opposing team’s localities).

I believe the reason that NFL teams have been able to play in UK up to now without forming a UK entity is that until now, the games have been exhibitions – no team has been a permanent home team.

Regarding the additional income taxes in London: in general, when companies send UK employees overseas for temporary assignments, the company incurs the additional income tax. Usually, the company will pay for a CPA to calculate the income tax difference between working in the US and working in the foreign country. The company will then reimburse the employee for the difference in income taxes. This reimbursement would likely fall into the benefits category of team spending, not the salary cap, so a London team wouldn’t be at a disadvantage for cap purposes.

Does the CBA extend to London?

In other words: is a US labor agreement valid in the UK? Yes and no. It would not be valid for a UK based company because that company would be subject to UK labor laws. It would work for the example I mentioned above. The Jaguars would employ all their players in Florida and would rent them to the UK subsidiary for “home” games.

What about health insurance in London?

Similar answer to the CBA answer above: the players would be employees of the US company and wouldn’t be eligible or obligated to use the UK health system.

For more information on the items above, google “cross border employment”.

Am I proposing that the salary cap should be different for each team?

No. For one, I don’t think there’s any traction within NFL teams or the league office to change. Second, taxes are just one difference. If the NFL adjusts the cap for tax differences, should it also adjust for city/metro population (fan base) or the size of local corporations able to sponsor the team/stadium?

Where does a player’s “state of residence” come into play?

Some states require that residents claim a state of residence on their income taxes. The states do not agree on how to determine a state of residence. Some criteria for different states are:

- State where a person spends 183+ days in a year.

- State where a person spends 183+ days and maintains a permanent residence.

- Same as above but permanent residence must be maintained for at least 11 months.

- State where a person’s “permanent residence” is located.

The reason a state of residence is important is some states claim authority to tax their residents’ income regardless of where it was earned. This means that a player that maintains a residence in Oregon and plays for a team in New York may end up having two states attempt to tax the same earnings. A player can get around this by maintaining their permanent residence in a state with no income taxes such as Florida or Texas. In that case, even if their state of residence “taxes” their annual income, the tax rate is 0%, so the player wouldn’t owe any additional taxes.

How do states determine how much income is earned in their state?

There is not a consensus among states on this matter. For the purposes of my earlier article, I assumed that 1/16th of each player’s salary was earned at the game site, which is an oversimplification of how each player’s earnings will eventually be taxed. The most common method I have found is the concept of days worked. Essentially, a state calculates your earnings in their state by dividing the number of days a player spent in their state by the total number of working days and multiples the result by a player’s annual earnings. The reason that can be complicated (and the reason I opted for the 1/16th method) is that there isn’t a concrete way to determine days worked. Take the Seahawks as an example:

Activity | # Days |

| Rookie Minicamp | 3 |

| Offseason Workouts | 36 |

| Minicamp | 3 |

| Training Camp | 33 |

| Regular Season | 118 |

| Total Days worked | 193 |

**Update 10/14/16: the chart above was originally published showing offseason workouts at 9 days rather than 9 weeks @ 4 days a week.**

Did a player earn his salary over 118 regular season days, 193 total days (190 for non-rookies), or some other total such as total days from the start of offseason workouts to the end of the regular season? Players in low or no income tax states want to use a higher total because more of the non-regular season time is spent in their team facilities. Players in high income tax states want to use the lower possible number so that the least amount is applied to their team’s state.

This also applies to endorsement deals. If a player is paid by Nike, Reebok, UnderArmour, Gatorade, etc, that deal is earned throughout the year. If a player is in California for 3 road games (~6-10 days), California’s Franchise Tax Board will want a portion of the endorsement earnings.

Suppose we eliminate everything but the regular season days (Monday before first game 9/5/16, last game 1/1/17). That means that a Seahawks player that is on the roster for the entire regular season will earn his salary over the course of approximately 118 days. Let’s assume that the Seahawks play their away games against New England and Jets in consecutive weeks (instead of Weeks 4 and 10). The team could be in Massachusetts and New Jersey for as few as 4 days if for each game they fly in on Saturday morning and back to Seattle after the game on Sunday. They could also be in the northeast for up to 8 days if they decide to remain local after the first game instead of flying back to Seattle in between games.

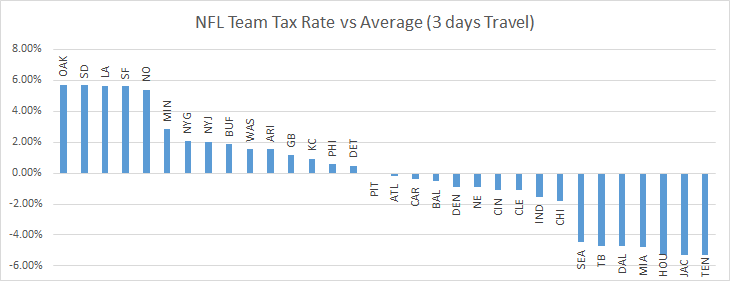

Assuming that each team only travels to the game site for 3 days for each away game, the blended tax rates by team would look closer to this:

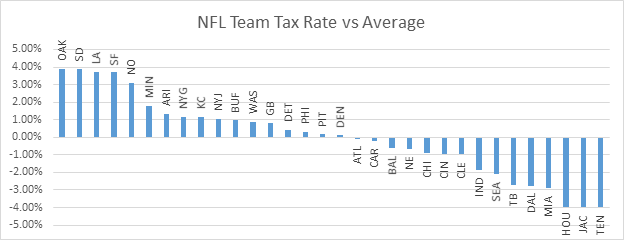

Original Chart from prior article:

The end result is the high teams are about 1% higher than under the previous model and the low teams are about 1% lower. However, the overall picture is essentially unchanged.

One commenter to the prior article noted a trick that Washington uses to get out of Maryland taxes. Washington practices and stays overnight in Virginia, then travels across the border to Maryland for the game. Since the players aren’t in the state for over 24 hours, they aren’t subject to Maryland taxes. There may be other similar situations for other game sites.

Does is matter if players are W-2 employees or 1099 consultants?

W-2 vs 1099 status does not affect where you owe taxes – the same rule of “location of the work performed/income earned” applies. The difference lies in the amount. Individuals that work as 1099s instead of W-2 employees pay both the employer and employee portion of payroll taxes and would be responsible for sending estimated income tax payments to the IRS and states. W-2 employees only pay the employee portion of payroll taxes (social security, Medicare, some local taxes) and have the remittance portion of the process handled by the employer through payroll deductions.

How do “Jock Taxes” come into this?

Jock taxes can be two different situations: (1) taxes that only apply to athletes, and (2) taxes that apply to everyone but are only enforced against athletes. If any resident of Seattle travels to Los Angeles for a short period of time to work, they may be subjected to taxes. However, if the amount to be taxed is small, most states won’t chase you down (and may not know you were in the state at all) and most companies won’t change their payroll deductions to reflect the temporary work assignment. High profile individuals like athletes, musicians, politicians (and others giving speeches), and others appear to be targeted for additional taxes because (1) the amount earned is easily calculated and likely a large amount, (2) the work schedule of the individual is easily traceable, and (3) both (1) and (2) are likely public knowledge. While I have read that many state or cities have jock taxes, they seem to be getting phased out as more and more individuals sue the tax departments of different states for (allegedly) levying unconstitutional taxes against them. When you read the term “jock taxes” in reference to out of state taxes, you are most likely reading about selective enforcement rather than a tax that only applies to athletes.